Tax Changes Could Bring More Donors — But Less Charitable Giving

Nonprofits may finally solve one of their biggest challenges — declining donor participation. But it could come at a cost.

A new analysis from the Indiana University Lilly Family School of Philanthropy, “The Philanthropy Outlook: Estimating Effects on Charitable Giving From the One Big Beautiful Bill,” estimates that recent tax changes could bring millions of new donors into the sector while reducing total charitable giving by about $5.7 billion annually. Depending on how donors respond, the impact could range from a $2.5 billion decline to as much as $11.7 billion.

The report is grounded in a core concept: Tax policy changes the “price of giving,” or the after-tax cost of donating, which in turn influences donor behavior. The estimates draw on established research and data sources.

That tension — more donors, but less total giving — highlights how changes to the tax code are reshaping not just how much people give, but who gives and how.

“Tax policy changes shape charitable giving, and their effects vary across different policies, types of donors, and ways of giving,” Patrick M. Rooney, Ph.D., professor emeritus of philanthropic studies and economics at the Lilly Family School of Philanthropy, said in a statement. “Changes that affect high-income households and large corporate donors have the greatest influence on total giving levels. Policies that broaden incentives to give, such as the newly enacted universal charitable deduction, are likely to increase the number of people who give.”

Tax Policy Shift Could Help Reverse Donor Decline

For a sector that has seen donor participation decline over time, the provision represents a structural attempt to bring more households into the giving base. The new analysis suggests that goal may be within reach.

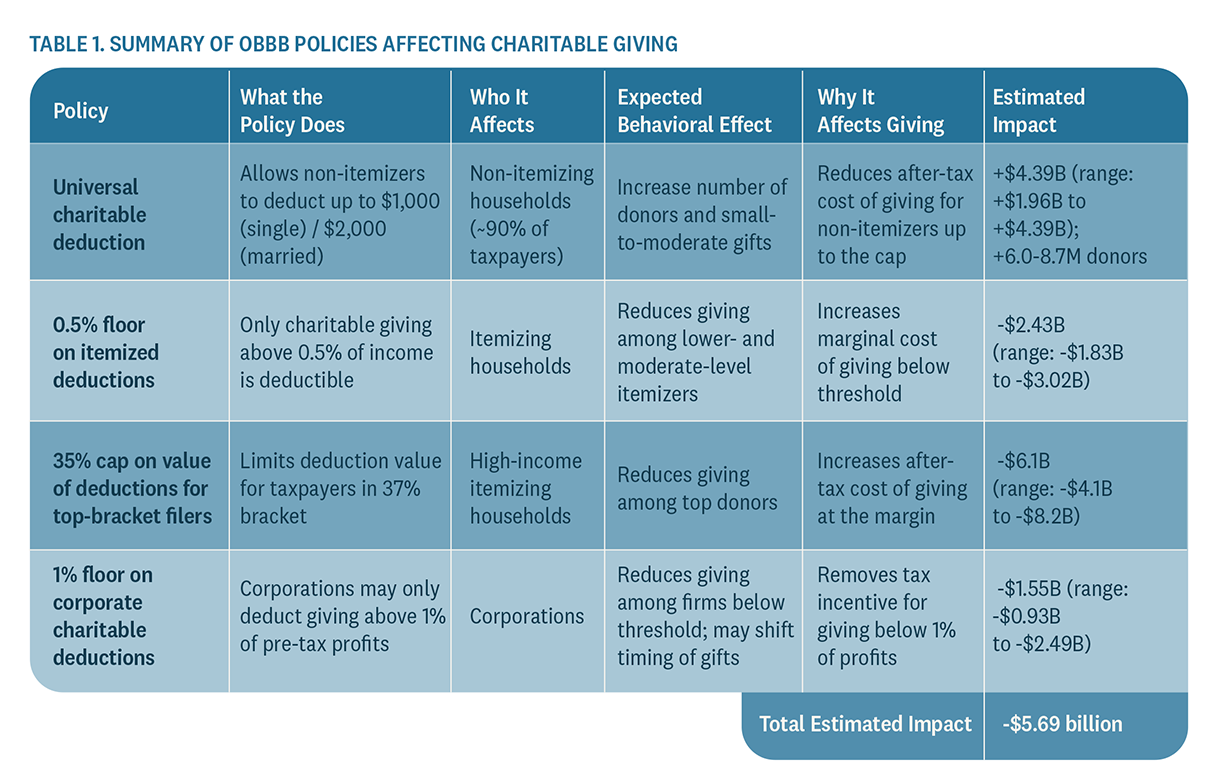

Among the most notable provisions is a new universal charitable deduction for non-itemizers, which allows taxpayers who take the standard deduction to deduct up to $1,000 in charitable contributions (or $2,000 for married couples filing jointly).

The universal charitable deduction is expected to increase the number of donor households by between 6 million and 8.7 million, and generate up to $4.4 billion in additional giving annually. The report also estimates that about $62.5 billion could be newly reported for tax purposes, reflecting existing giving that previously went undeducted and strengthening giving data, which relies heavily on IRS tax return information.

However, donor behavior may take time to adjust. Following the 2017 Tax Cuts and Jobs Act, which increased the standard deduction and reduced the number of itemizers, giving patterns shifted gradually as households responded to new incentives.

That increase in giving also has limits. While 90% of households do not itemize, roughly 85% of those non-itemizing households give below the deduction caps, meaning most donors will experience a direct change in the cost of giving. Those households represent a broad share of potential donors, but typically contribute smaller amounts, which limits the policy’s effect on overall charitable dollars.

A much smaller share of households — those giving above the cap — account for a disproportionate share of total dollars, limiting the policy’s ability to drive overall revenue growth. Giving from these households is only expected to climb by about $45 per household, but across roughly 116 million non-itemizing households, those modest increases scale to billions in additional giving.

Why More Donors May Still Mean Less Charitable Giving

The universal deduction increases participation, but other provisions in the law move in the opposite direction — particularly when it comes to philanthropy among high-income donors and corporations.

A cap on the value of itemized deductions for top earners is projected to reduce charitable giving by approximately $6.1 billion annually, while a new 0.5% floor on itemized deductions is expected to further reduce giving by about $2.4 billion. Meanwhile, changes to corporate deduction rules could reduce giving by another $1.6 billion.

These changes matter because high-income households account for a disproportionate share of charitable giving, and the report notes they are also more responsive to changes in tax incentives. Because they tend to give larger gifts and plan their giving more strategically, even modest increases in the after-tax cost of giving can lead to significant shifts in behavior.

For example, households with adjusted gross income of $500,000 or more accounted for about 57% of itemized charitable giving in 2022, according to IRS data cited in the report. As a result, only about 1.7% of itemized charitable giving falls below the 0.5% of income threshold, limiting the impact of that provision.

The same pattern holds in the corporate sector. Researchers estimate that about 26% of corporate giving could lose its deductibility under the new 1% floor. But despite more than 70% of companies giving less than 1% of their pre-tax profits — and losing tax incentives under the new rules — the majority of corporate giving is concentrated among a much smaller group of companies. That concentration limits the overall impact of new incentives while amplifying the effect of changes among top contributors.

New tax policy could expand the donor base in 2026, even as total charitable giving declines, according to a new analysis.

What the Tax Changes Mean for Nonprofits

The result is a mismatch between donor growth and revenue. The universal deduction brings more people into the giving ecosystem, but those contributions are typically smaller and may not fully offset declines in higher-value gifts. Meanwhile, relatively small changes in behavior among high-income donors and major corporations can outweigh gains from millions of smaller gifts.

Taken together, these changes reflect concerns the sector raised as the legislation moved through Congress. With 66% of total giving in 2024 — the latest year for which Giving USA data is available — coming from individuals and 7.5% from corporations, this bill may affect nearly three-quarters of giving.

For nonprofits, the implications are less about a simple decline in giving and more about a shift in how giving is structured. As organizations respond to changes in charitable giving tied to the “One Big Beautiful Bill Act,” some donors may adjust the timing or structure of their gifts to preserve tax advantages, according to researchers. Gift bunching may become more common, and corporations may shift strategies, including bunching contributions to corporate foundations and donor-advised funds.

This combination of offsetting incentives, varied donor responses, and delayed behavioral changes introduces a new level of uncertainty into charitable giving.

In 2026, nonprofits may need to navigate greater variability in charitable giving. As tax policy reshapes incentives, nonprofits could see more people entering the donor base. A broader base of smaller donors can strengthen long-term sustainability, deepen engagement, and build a pipeline for future major giving. At the same time, charitable giving is expected to decline. The result is a more complex fundraising landscape where participation grows, even as revenue remains harder to predict.

- People:

- Patrick M. Rooney